Click here for full Monthly Property Report

Despite a dip in April sales activity, most regions remained relatively steady with broader market conditions largely unchanged. Overall, the number of sales remains close to the long-term April average, highlighting that this year’s softer headline result still sits comfortably within the market’s historical range.

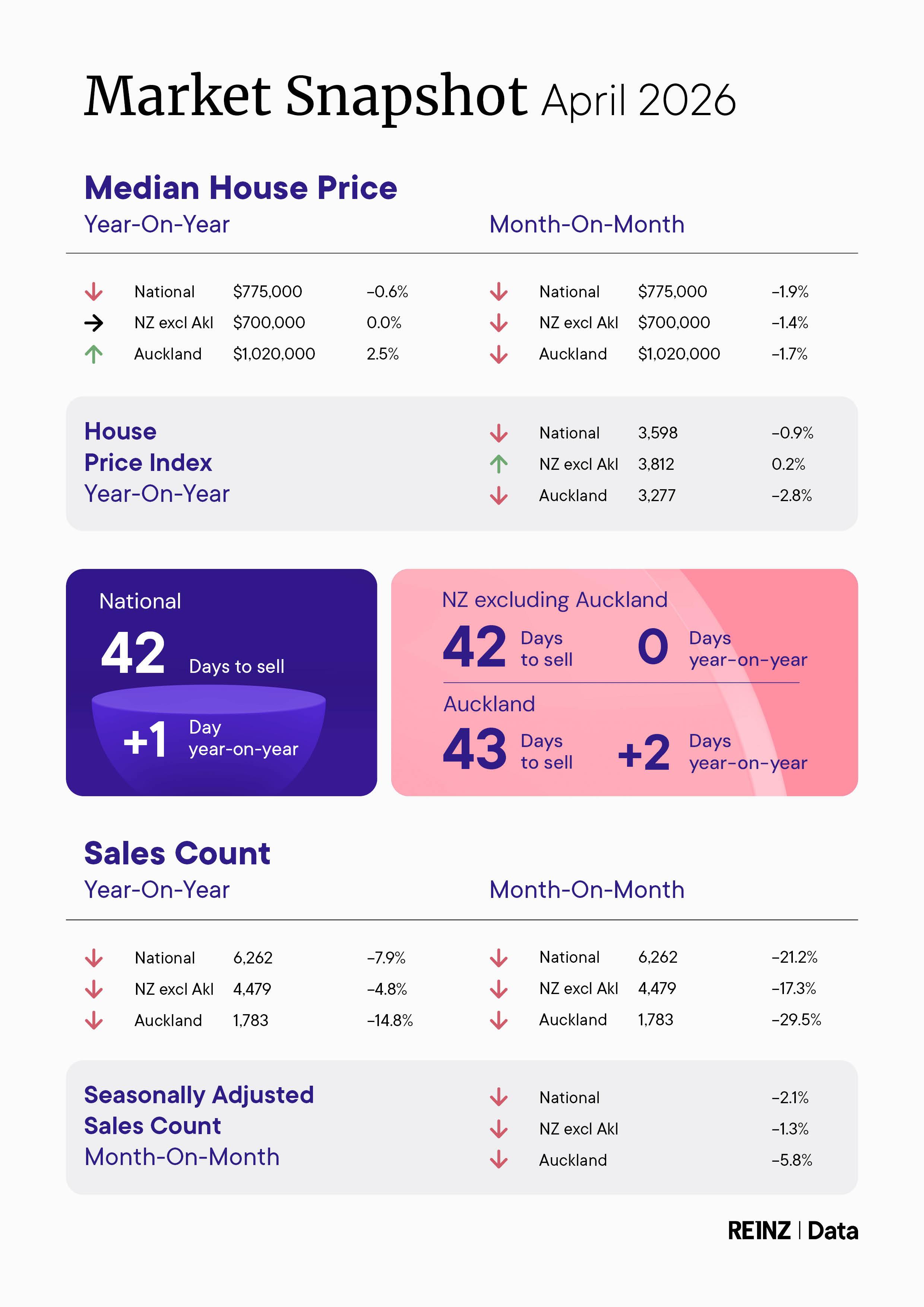

Data released today by the Real Estate Institute of New Zealand (REINZ) in its Property Report for April 2026 shows that national sales fell 7.9% year-on-year, yet the total of 6,262 represents a genuine, if modest, decline – with both April 2025 and April 2026 sitting close to the historical midpoint of every April since REINZ began tracking this data in 1992. April 2025 ranked 15th of 35 in that dataset; April 2026 ranks 18th.

The market showed a steadier pace through April. The seasonally adjusted sales count declined 2.1% compared to March – a more moderate signal than the raw month-on-month drop of 21.2%, most of which is seasonal. It suggests buyers remain active but measured, responding to cost-of-living pressure rather than stepping away from the market.

April 2026 marks the first clear sign that the combined weight of cost-of-living pressures – higher fuel costs, food prices, insurance, and local body rates – began influencing buyer decisions in a meaningful way. The impact was not uniform, however. Regions with higher vehicle dependency and lower median household incomes, including Hawke's Bay, Manawatu-Whanganui, and Marlborough, saw the largest softening in activity, consistent with pump prices hitting household budgets most directly in those areas. Canterbury, Southland, and Otago continued to record solid sales activity, though this reflects the relative strength of their local market fundamentals rather than any insulation from cost pressures.

April lands the housing market in a testing mid-cycle position: past the initial shock of the overseas conflict, into its cost-of-living pass-through, and now facing a potential OCR hike environment through winter. Fuel costs are amplifying regional differences, particularly in vehicle-dependent areas, against a broader backdrop of rising living costs, including food, insurance, and rates.

Election years in New Zealand have typically brought slower decision‑making from vendors and longer selling times, rather than sharp movements in prices. This uncertainty is weighing more heavily on Wellington due to its public sector exposure.

Looking at the House Price Index (HPI), which provides a more accurate measure of underlying value trends, Southland reached a new all-time HPI high, up 8.0% annually – the strongest growth of any region nationally. Canterbury runs at +3.0% annually, second highest nationally. The national HPI is down 0.9% year-on-year to 3,598, sitting 15.9% below its peak.

Auckland's HPI is down 2.8% annually but its three-month median of $1,022,000 is up 1.2% YOY, suggesting value stabilisation rather than decline. Wellington’s HPI declined by 2.5% annually while the regions inventory has risen sharply to 19 weeks from 14, the largest year-on-year increase in unsold stock of any major market nationally.

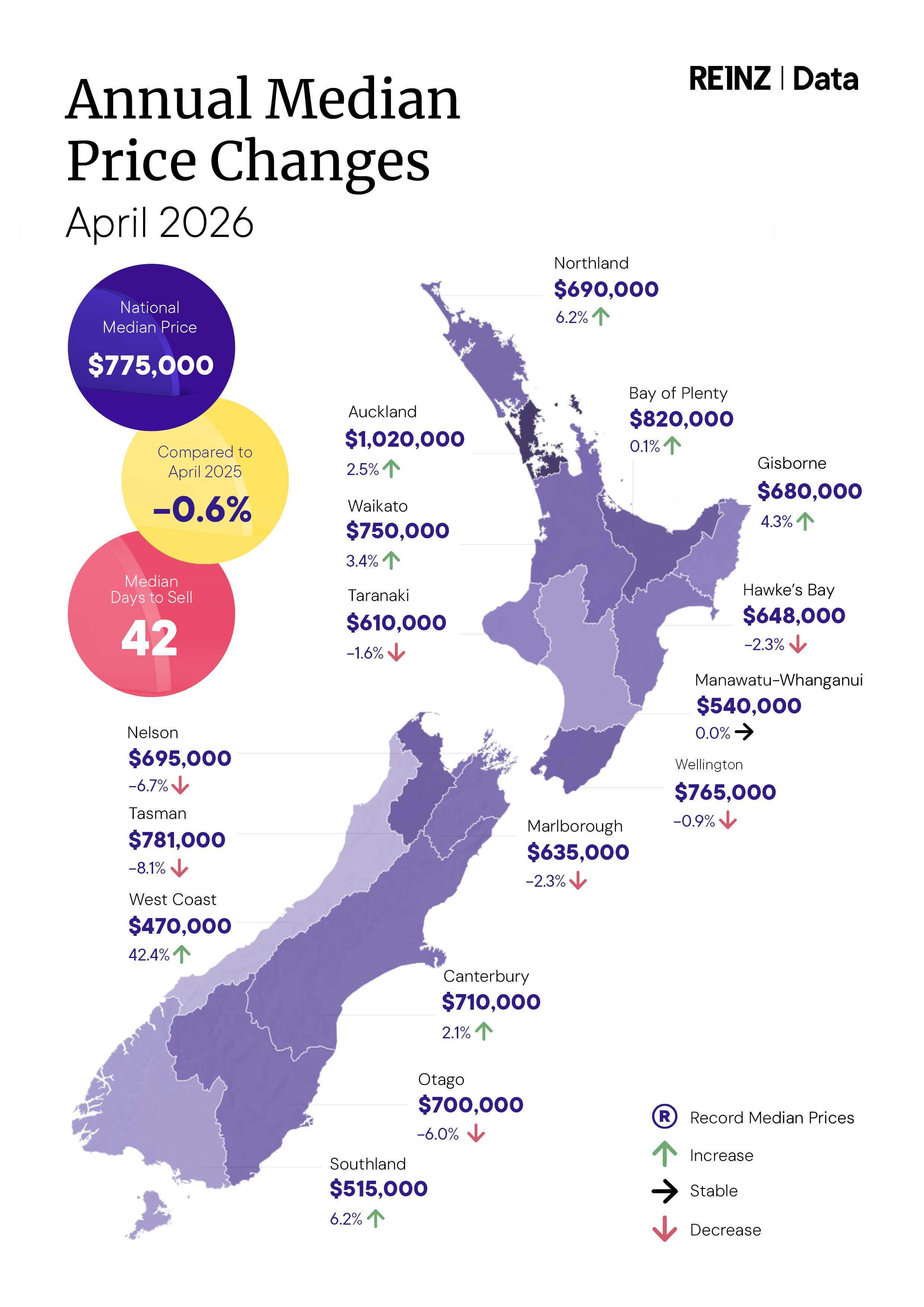

At the national level, the figures point to a stable market, though conditions vary by region. The median price eased slightly by 0.6% year-on-year to $775,000. Meanwhile, excluding Auckland, median prices were the same as in April 2025, at $700,000.

The uneven nature of the current market is clear with performance continuing to vary widely by region. Eight of the sixteen regions recorded year-on-year increases in median prices. The most substantive gains were in Southland and Northland (both +6.2%), Gisborne (+4.3%), and Waikato (+3.4%). The West Coast recorded a sharp single-month lift of +42.4% to $470,000, though this is based on only 47 sales and should be considered in context. Tasman, Nelson, and parts of the North Island recorded softer results. The three-month median of $785,000 is up 0.6% year-on-year and provides a clearer indication of underlying price movement.

National inventory levels* rose by 3.9% from last year to 37,334 properties. Supply levels moved in both directions over April, with a sharp incline on an annual basis, but down month-on-month. New listings* increased 7.4% year-on-year to 9,139 while excluding Auckland there was a slight decline of 0.4%, with 5,717 new listings. National monthly movements saw a decline of 24.2%.

Median Days to Sell remained steady throughout April, with properties taking a median of 42 days nationally – only a one-day increase compared to last year. Excluding Auckland, the median was also 42 days and saw no change year-on-year and month-on-month.

The auction market sustained its share. Nationally, 14.1% of sales were via auction, up from 13.7% in April 2025. Auckland held a 22.9% auction share (slightly lower than last year’s 23.9%), and Canterbury lifted to 19.2% from 17.4%. The strong use of auctions highlights ongoing confidence from vendors and salespeople in competitive sales processes.

RBNZ kept the OCR at 2.25% in April but signalled that rate rises would follow should core inflation fail to ease toward 2%. Most major bank economists now consider an OCR hike this year a probability rather than a possibility as ANZ, ASB, Westpac, and Infometrics have all brought forward their hike forecasts with some anticipating the first move as early as the 27 May MPS.

For the housing market, this shift from a cutting environment to an imminent-hike environment removes the tailwind of falling rate expectations that underpinned 2025's recovery, and begins to introduce the prospect of new serviceability pressure - a meaningful change from April's starting position. The key question for May and June is whether listings continue to build faster than sales can absorb them as we move into winter.

ENDS

*Inventory and Listings data courtesy of realestate.co.nz

Media contact:

Communications and Engagement Team

[email protected]

Fact sheet

National Highlights for April

- The total number of properties sold in New Zealand decreased by 7.9% year-on-year, from 6,797 to 6,262 sales. New Zealand, excluding Auckland, declined by 4.8% year-on-year, from 4,704 to 4,479.

- Nationally, the seasonally adjusted figures for New Zealand show a sales count decrease of 2.1% compared to March. Seasonally adjusted sales figures for New Zealand, excluding Auckland, show a 1.3% month-on-month decrease.

- Listings* nationwide increased by 7.3% year-on-year, reaching 9,139 new listings. For New Zealand, excluding Auckland, new listings decreased by 0.4%, at 5,717.

- The median Days to Sell for New Zealand increased by one day to 42 days. Excluding Auckland, the median Days to Sell was the same as the previous year, at 42 days.

Regional Highlights

- Eight of the sixteen regions recorded year-on-year increases in median prices; the highest increases were observed in:

o West Coast, up 42.4% to $470,000 (based on 47 sales — interpret with caution)

o Southland, up 6.2% to $515,000

o Northland, up 6.2% to $690,000

o Gisborne, up 4.3% to $680,000

- Four regions recorded an increase in sales compared to April 2025. Those four regions were:

o West Coast, up 30.6% to 47 sales

o Southland, up 17.9% to 184 sales

o Taranaki, up 7.7% to 181 sales

o Otago, up 1.3% to 398 sales

*Inventory and Listings data courtesy of realestate.co.nz

More information on activity by region can be found in the regional commentaries on the REINZ's Website.

Median Prices

- Eight of the sixteen regions recorded a year-on-year rise in the median price, with West Coast showing the strongest growth at 42.4%.

- Across Auckland’s seven territorial authorities, four recorded an increase compared with April 2025, with Rodney District showing the largest lift at 9.1%.

- In Wellington, three of the eight territorial authorities saw an annual increase, led by Upper Hutt City at 9.4%.

- MacKenzie District reached a new all-time territorial authority median price record this month: $1,150,000, beating the previous high of $930,595 recorded in January 2026.

Sales Counts

For the month of April

- Otago, Southland and Taranaki had their highest number of sales since 2016

- West Coast had its highest number of sales since 2021 which was its equal. It was 2006 when West Coast last had a higher sales count in April.

Median Days to Sell

For the month of April

- Canterbury had its highest median Days to Sell since 2011

- Southland had its lowest median Days to Sell since 2021

House Price Index (HPI)

- Southland recorded the strongest HPI movement year-on-year, increasing 8.0%, ahead of Canterbury (3.0%) and Otago (2.0%).

- Over the three months to April, Bay of Plenty showed the highest HPI growth nationwide at 2.4%, followed by Canterbury (2.2%) and Southland (0.9%).

- Southland's HPI reached a new all-time high this month — the only region nationally to do so.

- New Zealand HPI year-on-year change is a decrease of -0.9%, a worsening from the 0.2% increase reported last month

Inventory

- Inventory increased year-on-year in ten of the fifteen included regions

- Auckland and Wellington have each experienced 27 consecutive months of year-on-year inventory growth.

Listings

- Inventory increased year-on-year in ten of the fifteen included regions

- Auckland and Wellington have each experienced 27 consecutive months of year-on-year inventory growth

Auctions

- In New Zealand, there were 880 auction sales (14.1% of all sales) in April 2026. For the same period last year, there were 929 auction sales (13.7% of all sales).

More information on activity by region can be found in the regional commentaries visit the REINZ’s website.